Bulletins and News Discussion from December 23rd to December 29th, 2024 - The War on Christmas: Hypersonic Holidays

Bulletins and News Discussion from December 23rd to December 29th, 2024 - The War on Christmas: Hypersonic Holidays

Image is from Futurama.

Happy holidays, fellow godless communists. We are in year three of the Five-Year Plan to eliminate all Christmas cheer and create a world free of the joys and festivity of Christmas. Nobody should have to be reminded that in our concrete brutalist communist strongholds, NO ornaments are allowed in December. Please report any Christmas trees, snowflakes, baubles, and presents to the evil secret police, and anybody caught violating their Volcel Pledge by having a tentative kiss under a mistletoe will be shot on sight.

Developments lately have been grim. Our Supreme Communist Dictator Brandon is being removed from office by Christmas-loving patriots, and soon, Christmas will adorn the White House for another four years. This is obviously very disappointing, but while Christmas joy is strictly prohibited, good vibes are still strongly encouraged. Revolutionary optimism (a term we only bring out when things are going very badly and we need to be delusional) shall triumph over defeatist rhetoric by stooges of the Christmas regime.

We must have hope. Our foreign allies aiding us in destroying Christmas now possess hypersonic weaponry, allowing us to compete with and overcome the engine technology powering Santa's sleigh. Abroad, they have destroyed factories and hit cities with missiles travelling at unimaginable speeds into precise targets, while the Christmas regime struggles to produce their own such missiles, as they are still reliant on aircraft bombing campaigns. Precision has a quality all its own, or something along those lines. We just have to hold out another two years or so, and I swear to you: we will live in a world without this accursed holiday.

No current struggle session discussion here in the news megathread please, you will be banned from the comm and your comment will be removed.

Please check out the HexAtlas!

The bulletins site is here!

The RSS feed is here.

Last week's thread is here.

Israel-Palestine Conflict

Sources on the fighting in Palestine against Israel. In general, CW for footage of battles, explosions, dead people, and so on:

UNRWA reports on Israel's destruction and siege of Gaza and the West Bank.

English-language Palestinian Marxist-Leninist twitter account. Alt here.

English-language twitter account that collates news.

Arab-language twitter account with videos and images of fighting.

English-language (with some Arab retweets) Twitter account based in Lebanon. - Telegram is @IbnRiad.

English-language Palestinian Twitter account which reports on news from the Resistance Axis. - Telegram is @EyesOnSouth.

English-language Twitter account in the same group as the previous two. - Telegram here.

English-language PalestineResist telegram channel.

More telegram channels here for those interested.

Russia-Ukraine Conflict

Examples of Ukrainian Nazis and fascists

Examples of racism/euro-centrism during the Russia-Ukraine conflict

Sources:

Defense Politics Asia's youtube channel and their map. Their youtube channel has substantially diminished in quality but the map is still useful.

Moon of Alabama, which tends to have interesting analysis. Avoid the comment section.

Understanding War and the Saker: reactionary sources that have occasional insights on the war.

Alexander Mercouris, who does daily videos on the conflict. While he is a reactionary and surrounds himself with likeminded people, his daily update videos are relatively brainworm-free and good if you don't want to follow Russian telegram channels to get news. He also co-hosts The Duran, which is more explicitly conservative, racist, sexist, transphobic, anti-communist, etc when guests are invited on, but is just about tolerable when it's just the two of them if you want a little more analysis.

Simplicius, who publishes on Substack. Like others, his political analysis should be soundly ignored, but his knowledge of weaponry and military strategy is generally quite good.

On the ground: Patrick Lancaster, an independent and very good journalist reporting in the warzone on the separatists' side.

Unedited videos of Russian/Ukrainian press conferences and speeches.

Pro-Russian Telegram Channels:

Again, CW for anti-LGBT and racist, sexist, etc speech, as well as combat footage.

https://t.me/aleksandr_skif ~ DPR's former Defense Minister and Colonel in the DPR's forces. Russian language.

https://t.me/Slavyangrad ~ A few different pro-Russian people gather frequent content for this channel (~100 posts per day), some socialist, but all socially reactionary. If you can only tolerate using one Russian telegram channel, I would recommend this one.

https://t.me/s/levigodman ~ Does daily update posts.

https://t.me/patricklancasternewstoday ~ Patrick Lancaster's telegram channel.

https://t.me/gonzowarr ~ A big Russian commentator.

https://t.me/rybar ~ One of, if not the, biggest Russian telegram channels focussing on the war out there. Actually quite balanced, maybe even pessimistic about Russia. Produces interesting and useful maps.

https://t.me/epoddubny ~ Russian language.

https://t.me/boris_rozhin ~ Russian language.

https://t.me/mod_russia_en ~ Russian Ministry of Defense. Does daily, if rather bland updates on the number of Ukrainians killed, etc. The figures appear to be approximately accurate; if you want, reduce all numbers by 25% as a 'propaganda tax', if you don't believe them. Does not cover everything, for obvious reasons, and virtually never details Russian losses.

https://t.me/UkraineHumanRightsAbuses ~ Pro-Russian, documents abuses that Ukraine commits.

Pro-Ukraine Telegram Channels:

Almost every Western media outlet.

https://discord.gg/projectowl ~ Pro-Ukrainian OSINT Discord.

https://t.me/ice_inii ~ Alleged Ukrainian account with a rather cynical take on the entire thing.

You're viewing a single thread.

https://archive.is/WjBbA(from FT)

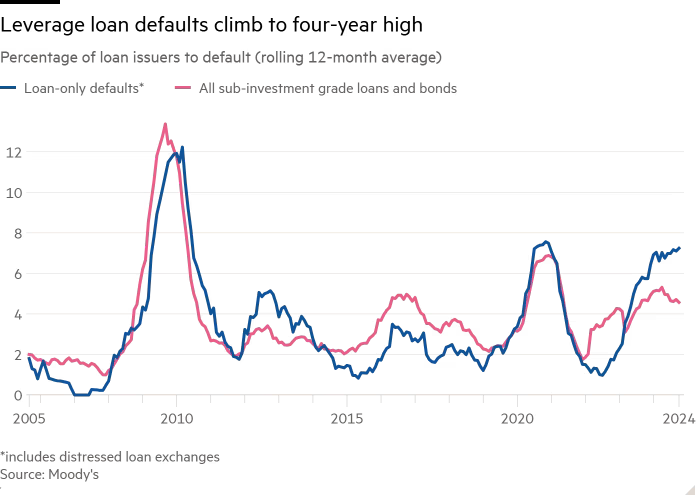

Defaults on leveraged loans soar to highest in 4 years

US companies are defaulting on junk loans at the fastest rate in four years, as they struggle to refinance a wave of cheap borrowing that followed the Covid pandemic. Defaults in the global leveraged loan market — the bulk of which is in the US — picked up to 7.2 per cent in the 12 months to October, as high interest rates took their toll on heavily indebted businesses, according to a report from Moody’s. That is the highest rate since the end of 2020.

The rise in companies struggling to repay loans contrasts with a much more modest rise in defaults in the high-yield bond market, highlighting how many of the riskier borrowers in corporate America have gravitated towards the fast-growing loan market.

Because leveraged loans — high yield bank loans that have been sold on to other investors — have floating interest rates, many of those companies that took on debt when rates were ultra low during the pandemic have struggled under high borrowing costs in recent years. Many are now showing signs of pain even as the Federal Reserve brings rates back down. “There was a lot of issuance in the low interest rate environment and the high rate stress needed time to surface,” said David Mechlin, credit portfolio manager at UBS Asset Management. “This [default trend] could continue into 2025.”

Punitive borrowing costs, together with lighter covenants, are leading borrowers to seek other ways to extend this debt. In the US, default rates on junk loans have soared to decade highs, according to Moody’s data. The prospect of rates staying higher for longer — the Federal Reserve last week signalled a slower pace of easing next year — could keep upward pressure on default rates, say analysts.

Many of these defaults have involved so-called distressed loan exchanges. In such deals, loan terms are changed and maturities extended as a way of enabling a borrower to avoid bankruptcy, but investors are paid back less.

Such deals account for more than half of defaults this year, a historical high, according to Ruth Yang, head of private market analytics at S&P Global Ratings. “When [a debt exchange] impairs the lender it really counts as a default,” she said.

“A number of the lower rated loan-only companies that could not tap public or private markets had to restructure their debt in 2024, resulting in higher loan default rates than those of high-yield bonds,” Moody’s wrote in its report. Portfolio managers worry that these higher default rates are the result of changes in the leveraged loan market in recent years. “We’ve had a decade of uncapped growth in the leveraged loan market,” said Mike Scott, a senior high yield fund manager at Man Group. Many of the new borrowers in sectors such as healthcare and software were relatively light on assets, meaning that investors were likely to recover a smaller slice of their outlay in the event of a default, he added.

“[There has been] a wicked combination of a lack of growth and a lack of assets to recover,” thinks Justin McGowan, corporate credit partner at Cheyne Capital. Despite the rise in defaults, spreads in the high-yield bond market are historically tight, the least since 2007 according to Ice BofA data, in a sign of investors’ appetite for yield. “Where the market is now, we are pricing in exuberance,” said Scott.

Still, some fund managers think the spike in default rates will be shortlived, given that Fed rates are now falling. The US central bank cut its benchmark rate this month for the third meeting in a row. Brian Barnhurst, global head of credit research at PGIM, said lower borrowing costs should bring relief to companies that had borrowed in the loan or high-yield bond markets.

Jay Powell speaks at a press conference “We don’t see a pick-up in defaults across either asset class,” he said. “To be honest, that relationship [between leveraged loans and high-yield bond default rates] diverged probably in late 2023.”

But others worry that distressed exchanges hint at underlying stresses and only put off problems until a later date. “[It’s] all well and good kicking the can down the road when that road goes downhill,” noted Duncan Sankey, head of credit research at Cheyne, referring to when conditions were more favourable for borrowers. Some analysts blame loosening credit restrictions in loan documentation in recent years for allowing an increase in distressed exchanges that hurt lenders. “You can’t put the genie back in the bottle. Weakened [documentation] quality has really changed the landscape, in favour of the borrower,” said S&P’s Yang.

Its been baking for decades but it will be the primary focus of the next financial crisis.

Many of these defaults have involved so-called distressed loan exchanges. In such deals, loan terms are changed and maturities extended as a way of enabling a borrower to avoid bankruptcy, but investors are paid back less.

These distressed exchanges operate in a legal grey area and intentionally favor larger lenders. Smaller lenders will be exchanged in to new loans with haircuts and no collateral while the majority lenders get new secured debt. As defaults rise this will continue to contribute to more centralization and accumulation by the largest firms. Typical infighting among the clergy in their religious institutions.